A Freelancer’s Guide to Preparing for Retirement

Life is tough as a freelancer, especially when it comes to planning for the future. Today we’re going to discuss some hard facts about how to financially prepare for your retirement on your own.

You won’t find an article filled with vague tips on being frugal, instead we’ll introduce you to some basic financial instruments that you should be familiar with so you can decide which are best for you.

Why Freelancers Don’t Want to Talk About This

You’re a freelancer. You work where you want, when you want for who you want. You’re making more and are happier than you could ever be at any design firm. But those guys sitting behind a corporate desk have a few things you envy don’t they? One of these things is a professional parachute. They have an escape plan that says when they reach a certain age, they can kick back and play golf while drawing a nice little monthly sum to hold them over until it’s time to visit the mortician.

Countless freelancers are caught up in “here and now” thinking and give little to no thought towards how to retire. We have it in our minds that we’ll simply work until we’re dead. However, if you could go forward in time and have a discussion with your 65 year old self, he/she would no doubt offer different advice: start preparing as soon as possible.

Retirement is an unpleasant topic for freelancers. Forget the fact that we’re young, tech savvy individuals that can’t stand the idea of getting old and calling our grandkids to come program our universal remotes, even more depressing is the realization that we’re creative people who often have trouble grasping the financial world.

Stocks, bonds, mutual funds, IRAs, 401ks, hold on there buddy, if you want to speak my language you have to talk about things like layer masks and drop shadows. This is the attitude that many freelancers take because these topics are frankly quite intimidating. Some people can go on and on about the long-term prospects of the price of grain in China and this kind of discussion is a real turn off to a group of people who are more concerned with what the iPad 3 will be like.

It’s easy to feel dumb when conversation turns to financial instruments. It’s a complicated field that people study daily for years before they learn enough to realize that they don’t know half of what they need to!

However, this is not an excuse to avoid the subject. You have a responsibility to yourself and to your family to establish a plan for the future if you don’t currently have an employer taking care of it for you (even then it’s a good idea to take extra steps).

Numbers That Should Scare You

To emphasize the importance of saving for retirement, I’m going to run the same little experiment that my college finance professor ran with me years ago.

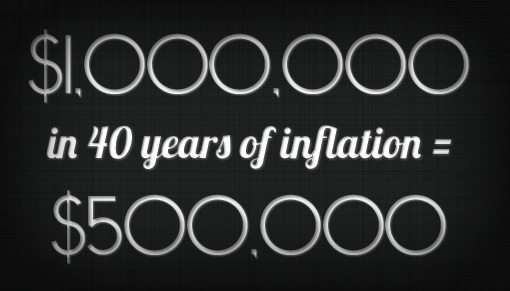

Think about how much you currently have saved for retirement. If you’re like most young freelancers, that number is at or close to $0. Now, let’s imagine that by some miracle, in the next 40 years you were able to squirrel away a whopping $1,000,000. So, the year is 2051, your retirement account has one million dollars and you make the grand announcement that you are retiring. You should be set right? I mean, you’re a freaking millionaire!

A Million Bucks Ain’t What It Used to Be

You’re forgetting about one nasty little beast: inflation. I can’t go into how every system works all over the world so we’ll have to use a standard, in this case American dollars and the American financial system (my apologies, this article will be quite biased towards U.S. readers). Our Federal Reserve Board of Governors, the people pulling the strings behind the scenes in the financial system, attempt to keep our inflation rate at around 2% per year. Speculation indicates that the real inflation rate is higher, but let’s go with this for now.

Using a simple inflation calculator, we see that at an average of two percent inflation per year, your $1,000,000 future dollars equate to around $500,000 of today’s dollars. As costs rise in the years to come, a dollar won’t go as far, hence equating the value of future dollars to something you understand: today’s dollars.

Can You Live on That?

So you thought you had $1,000,000, but in reality it’s more like $500,000. Your little nest egg was just cut in half! Let’s say you plan on living for twenty years after you retire, that gives you a measly $25,000 (in today’s dollars) to live on per year! Suddenly being a millionaire isn’t all it’s cracked up to be. This number gets much worse if the inflation rate averages around 4%. This turns your million bucks into around $210,000, which leaves you $10,500 for the next twenty years (tip: getting old costs a lot more than ten grand a year).

You might be tempted to think that there’s no way you can come up with this kind of money, but you’re wrong. Fortunately, because of the time value of money, interest and investment payoffs, if you start investing in your 20s, being a millionaire by the time you retire really is a completely reasonable goal!

Standard Retirement Accounts

The numbers above are discouraging, maybe enough so that they’ve only served to reinforce your idea that you simply can’t handle this retirement planning stuff. However, the desired effect is to show you the seriousness of the situation. If you plan on remaining a freelancer, you need to start figuring out how to save for your parachute.

The good news is that there are relatively few primary options that you need to consider. Financial products aimed at retirement are fairly established as an effective route and a little bit of education goes a long way towards choosing the right path for you. Let’s take a look at some terms that you’ve no doubt heard about before but are too proud to admit that you don’t quite understand!

Traditional IRA

This is a term I know you’re familiar with. IRA stands for Individual Retirement Account. Basically, an IRA is a device that was contrived for tax purposes. With a traditional IRA, you are allowed to stow away up to a few thousand dollars per year (usually around $5,000 but it varies depending on your income).

By placing this money into an IRA, it is actually deducted from your taxable income. Then, when you retire and remove the money from your IRA, it is taxed as income. If you’re a quick thinker, you might be tempted to think that this is pointless. Either it’s taxed now or later, either way it’s taxed right?

The benefit here is tax deferral. Let’s simplify the scenario to see how this works. Say I give you $1 per year to invest for 40 years. If you pay 30% taxes on that dollar every year, then you really only get to invest $0.70 every year. After ten years you’ll have $7 that will earn interest for the next 30 years.

However, if you don’t tax that dollar right away, your account will grow by a dollar each year and will earn more interest by virtue of having more in the account. This time after ten years you’ll have $10 that will earn interest for the next 30 years. Sure, you’re still taxed once you remove the money, but you were able to take advantage of the interest on a larger amount of money over a period of 40 years, which can really pay off.

Roth IRA

A Roth IRA is a popular instrument recommended to many people who don’t have access to an employer matching contribution 401k account. It’s a lot like the traditional IRA: both are long-term retirement accounts and both limit your contributions (equal to your earned income), but there are a few significant differences.

Unlike with the traditional IRA, your contributions to a Roth IRA aren’t tax deductible up front. However, on the upside, there is no additional taxation when you decide to retire and withdraw the money. The basic benefit here is that money sitting in your Roth IRA can grow tax-free over the life of the account. With a normal savings account, you have to report interest income to the government and pay taxes on it, Uncle Sam rewards you though if you commit to saving the money in an IRA by allowing earnings to go by untaxed.

The Trouble with IRA’s

IRA’s are fantastic investment opportunities, but there are downsides too. First of all, you are often penalized for pulling your money out early. If you put money into an IRA, plan on it staying there for a long time.

Another thing to watch out for is that all IRA’s aren’t created equal. The characteristics described above are generalizations. Some retirement accounts are better, some are worse. Be sure to read the fine print to see exactly how you’ll be taxed and what penalties you’ll incur if certain actions are taken.

IRA Investments

As I just pointed out, IRAs differ depending on who you receive them from. One of the most important aspects of how one IRA is different from the next is how the money will be invested over time.

IRAs can include options to invest in stocks, bonds, mutual funds, CDs, and more. Once again, these terms are can be a little fuzzy so let’s briefly go over them.

CDs

A CD is a Certificate of Deposit and is a fairly typical instrument used in conjunction with IRA’s. They are low-risk investments that pay a higher yield than a typical savings account because you’re committing to not touching the money for a specified number of years.

However, though they might yield a higher return than a savings account, CDs are fairly weak as your only long-term strategy because they can earn a lot less than other investment options. The reason for this is the low amount of risk. When investing, always keep these rules in mind:

- Low risk = low potential return

- High risk = high potential return

Again, since CD’s are at the lower end of the risk spectrum, you can’t expect to earn much from them. That doesn’t mean they aren’t useful, just keep your goals in mind when making a decision.

Stocks

Stocks are a piece of ownership of a company. They fluctuate in value depending on both the actual financial and perceived current and future performance of the company.

Stocks are risky business! A few years on Wall Street will teach you that the stock market is a beast that will eat you up and spit you out penniless. Some stocks are considered extremely safe, others are extremely volatile. Applying the rules we just learned, I’ll let you guess which has the higher payoff.

Bonds

A bond is basically a very specific type of loan. When you purchase a bond, whether it’s from a company or a government, you are giving them a loan for a specified amount of time. The interest rate, or coupon, determines the amount of money the bondholder will receive in addition to the principal amount borrowed.

Bonds expire on a specific date whereupon you will receive back the money you invested. Interest is generally fixed and paid in installments over the life of the bond.

Like CD’s, bonds are generally considered to be a safer investment. Which of course in turn means that you can expect a limited amount of return. There are such thing as high yield or “junk bonds” that have the potential to earn you more, but these are a bit more unstable and can’t always be trusted to yield a return.

Mutual Funds

Mutual Funds are one of the more interesting financial instruments available for newbie investors. These are essentially a pool of money from a large group of people that is meticulously managed by a team of investment professionals.

Mutual Funds take your money and utilize all of the instruments above to try to maximize your return. Each mutual fund is different and usually has a specified area of investment and/or very precise goals that the fund attempts to meet.

The benefits here are clear. First, your money is generally spread around in multiple areas, which is considered safer than placing all your bets on one particular company or investment. Also, someone does most of the work for you! It’s in the best interests of the fund managers to give you a high return, so they generally attempt to do exactly that.

As always, there are a downsides as well. Namely, you have to be sure you understand how you will be charged. Mutual funds can come with several fees so again you’re stuck reading the fine print to make sure you don’t get screwed. Obviously, you also have to place a large amount of trust in someone you may not know, which can definitely be a scary thing to do!

Conclusion: Which Investments Should You Choose?

Now that you’re familiar with basic retirement accounts and the need to begin saving as soon as possible, you should be better prepared to approach your situation. Keep in mind that IRA’s certainly aren’t the only option, they’re just a very popular choice that I chose to spend today focusing on while briefly mentioning other areas such as stocks and bonds.

The question you’re no doubt left with is, which IRA should you choose? This is the part where I can’t help you much. Your situation is very different from mine. The amount of risk you are willing to accept is no doubt very different than the amount than I’m willing to accept and the amount of money you can invest will absolutely vary from the amount that I can.

This article is meant to prepare you to go and speak to a financial advisor. Armed with the knowledge above, you can make a more informed decision about the options that you’ll be presented with. Make an appointment at your bank or another financial institution whose reputation you trust and ask about the options above.

Bottom line: you can in fact take significant steps to ensure that you don’t have to work until you’re dead. Yes, it’s intimidating and it does take a little work and education on your part, but it more than pays off in the end. It just might be one of the best decisions you ever make, so stop putting it off and get started!